Transcript: Matterport Insurance Claims: Flood/Fire Remediation/Restoration10445

Pages:

1

WGAN Forum WGAN ForumFounder & WGAN-TV Podcast Host Atlanta, Georgia |

DanSmigrod private msg quote post Address this user | |

| WGAN-TV: Matterport Meets and and Flood Insurance Claims: Remediation and Restoration with Matterport Director, Business Development and Head of Partnerships and New Market Development Tomer Poran (Thursday, 7 November 2019) Transcript: Matterport Meets Insurance Claims: Flood and Fire Remediation and Restoration Transcript - Hi all, I'm Dan Smigrod, founder of the We Get Around Network Forum. Today is Thursday, November 7, 2019, and you're watching WGAN-TV Live at 5. Our topic today, Matterport meets insurance. That would be insurance claims for fire, flood, the remediation and restoration process. I'm super excited about today's show. I've been through three floods in our house with my wife, so I've got a lot of things to ask Tomer about on this topic. Tomer, good to see you. - You too, Dan. - Tomer is Matterport Director, Business Development. He's also head of Partnerships and New Market Development and he's also an insurance subject matter expert for Matterport, so super-excited that you're on the show today, Tomer. Thanks so much. - Thank you very much. Very excited to be talking to your listeners today, Dan. - Terrific, and good to see you again. I mentioned at the top of the show that my wife and I have been through three separate floods. I thought I'd visit with you on one of them. I remember the date, it was December 26. That's actually our wedding anniversary, so my wife and I were scheduled to go out to dinner three years ago, December 26, 2016. And earlier in the day, I walked downstairs and my daylight office with carpet, the floor was all squishy. And it was not a good feeling. It was a lot of water. And it had been raining like cats and dogs for about 30 days in Atlanta, Georgia. And so actually I didn't quite know what to do. This was the first time that that ever happened. I called my friend Alan who had been through a flood and fire in his house. And so he quickly explained this remediation process. I called his remediation company. And amazingly, I think it was on a Sunday, within about an hour, a company showed up with the blowers, dehumidifiers, et cetera. And I guess they quickly assessed that we were having a leak coming through the roof. So in any event, the first thing they did was take a lot of pictures. Kind of just where they had spotted water and then they were putting up some devices up on the drywall and realizing there was water behind drywall, so picture, picture, picture, picture. And then the next thing I know, they're knocking into the drywalls, they're opening them up, they're setting up blowers, dryers, dehumidifiers, vacuums. We're in a 5,200 square foot house, three levels. The bottom level is a daylight basement where I have my office. It was really a mess, and I wasn't quite sure we were going to get to go out for our wedding anniversary dinner. But somehow miraculously that happened. So now this seemed like it was pre Matterport. Lots of photos. Where does Matterport fit in on that first thing? If they had pulled out a Matterport camera, what would they have done and why? - Yeah, so that stage is often referred to as the pre mitigation stage or in the insurance terms, FNOL, First Notice of Loss. And your story is a, I guess, one of two ways things could go down. One, policyholder notices damage to the property. They do one of two things mostly. One, call a restoration remediation emergency services. These go under many names. You might know some of the major national franchises like ServPro, you'll see their green trucks with the orange triangle driving around almost anywhere you are around the US. ServiceMaster, another well known brand. But there's quite a few of these. 911 Restoration, PuroClean. About a third of them are franchised, the rest are not. We estimate something between 10,000 to 20,000 of these type contractors around the US. But it's a global business. So one of two things happens. You call one of these guys. The other thing that I'd say probably in the majority of cases happens is people call their insurance. My house has flooded, Allstate or State Farm or whatever your insurer is. And the insurance would refer your claim to what's called a desk adjuster, an insurance adjuster. And they would actually contract out emergency services to go to your house. So those are the two things that happen after first notice of loss. Once to get to the point of... Once those folks end up reaching your house, usually who you'll be talking to is the project manager, the mitigation project manager. They're often doubling as an estimator. And I'll go into kind of what that means. But the first thing they would do with any claim, regardless of Matterport or non Matterport, is basically they worry about how to they get paid for this like any service provider. Except in this case, unlike many service providers that arrive in your home, you're not paying. It's the insurance carrier that's paying. And because of that, they need to get three things down, three big things, when they get to the house. One is the scope of the claim. And that means we need to rip out drywall, we need to remove furniture, we need to take down carpeting, we need to set up dehumidifiers because of certain moisture levels in the floor, wall, like you mentioned. These are all the actions that they need to take and those actions all carry a price tag. Removing a fridge, there's a price for that. Ripping out a square foot of carpeting, wall to wall carpeting, there's a price for that. There are over 20,000 possible line items all captured in a software estimating software, such as Xactimate is probably the most prominent definitely in the US form of estimating software, but there are others, Symbility, Symsol, and others. So basically, this estimating software captures all the different types of actions they could take. So that's one, and that's called the scope. Scoping out what you need to do. Number two is documentation. And that's what you referred to as photos. There's no way for the insurance carrier to ever compensate you as a contractor if you don't show not only say removed damaged window, removed broken window, you have to show me that window is broken and show me that window is broken is a sufficient enough manner for me to determine that you couldn't have fixed it. You needed to replace it. Replacing more expensive than fixing in most cases. That's often a common point of dispute between the carrier and the adjuster. So we touched two things. Saying what you did and capturing photos of it. But the third thing that is just as important is if I say I ripped out the carpeting or I had to paint your entire first floor or I had to move all the ceiling panels in your basement, that tells me nothing as the insurance carrier if I don't know how big your floor was, how much square footage of wall did you paint. So that third component is basically build a 3D model. And that's what they do. Within that same software, Xactimate, you have module called Sketch. And that sketch model is where the contractor, or more specifically the estimator, is going to place the 3D model of the structure. So they're very busy measuring your house as well. Now, granted, if this was a small claim, anything under $5,000, you're not gonna see them go into too much effort in 3D modeling your entire house. Because if it's a single room damage, and like the room I'm standing in now, and it's a really small claim like under $3,000, contractor's just going to say, well, this looks like a four by five room, and that's what they'll put it down in. As the carrier, it's going to pass. They're not going to look for too much proof on a claim that small. When you get to the larger claims... - Yeah, for us it was $41,000 plus some change. - Okay, then I guarantee you that they put in a lot of effort into measuring that, because if you think of most of the damage being structural and needing to fix your entire room from the foundation to the wall to maybe some of the systems, then their dimensions matter a lot. If that room that was flooded was 10 by 10 or 30 by 30, that could literally 3x the settlement size. So very, very important for them to know measurement. - Well, things got pretty expensive, I guess, because in our daylight basement, it's an open floor plan. So there's almost 2,000 square feet of uninterrupted space. It's not partitioned by doors. So what I learned was all of a sudden, oh, it's not just replacing the 10 by 10 carpet that was affected, it was let's call it 2,000 square feet of floor covering. I'll add to this, because it may be helpful as you're describing the next steps, is on the main level of the house where they determined that the drywall need to be opened up, when they opened up the wall in our dining room, there were no two by fours vertically in the corner. This was a systemic amount of water that had been going on for years and years and years without us knowing it. And literally the two by fours had disintegrated in the corner of the house where the dining room is, which led to the hardwood floors, which is about 1,500 square feet on the main level, all needed, again, this is all new to me, but maybe there was four square feet of where the floor had to be cut up related to the problem. And so all of a sudden, that meant there was, I guess, 15 square feet of hardwood floors that needed to be replaced. And then on the top level of the house, it wasn't so bad. It was really some painting and the mold, the molding. But I think as you described, it was really interesting, because they were measure, measure, measuring stuff, and my head was scratching a little bit, because I had this 3D model of the house that I had taken a Matterport 3D tour of the house, and I said, well, I have this stuff that maybe this would make it easier to trace over or to do measurements from. And no, no, we use this process called Xactimate and this is what we need to do. So that's kind of, I think, where they were. First they were documenting before they did anything. And then when they got done setting up all this stuff and knocking all the drywall out, then they started, I guess, I think that's when they did the measuring but then they did more of this pictures. - Yeah, so I guess it's a good leeway to enter Matterport into the scene. And talking to a lot of these guys and realizing what you're telling me you're taking photos and you're measuring the place. That seems like a great fit for what we do at Matterport. It's kind of how we got started in the industry. And what we do, therefore, as a value proposition for these guys at a very simple level was, hey, look at these two actions you do. We do them better and faster. And that was kind of a very simple way for us to enter into this market. But what we didn't realize, and we were solving a big problems in photos. You talk to most insurance adjusters, general adjusters, large loss adjusters, catastrophe adjusters, they'll tell you that photo documentation is one of their biggest pains because of the level of photography, the quality of photography, and the missing photography that's often found on a claim file that they have to work against. Not only does this pain them, but it causes a lot of back and forth. A lot of back and forth causes a lot of time delays. And time delays for everyone. Insurance carriers, and this is what we found going into this industry. Everyone on the claim wants to get it over with, literally. The policyholder, the contractor wants to be in and out and get paid, the insurance carrier wants this out of their claims pipeline. There's a lot of overhead associated with that pipeline. They wanted out. And obviously you as the homeowner want everyone out of your house and to continue living your life. Or if you're a store owner, to get back in business. So time here is critical. And I'll get back to that. So not only were we fixing this issue of poor photography and making everyone's life simple, but we were obviously getting rid of the measurement process. But more so you talk to contractors and adjusters all using Xactimate, they'll tell you that sketching, that process you do within Xactimate when you're 3D modeling the house, is extremely laborious, time consuming. The industry is at a very high shortage of skill set in it. So you're talking about something that is hard to do, takes a long time, cumbersome, and there's not a lot of people that can do it other than really trained estimators. Mediocre ones do it in a mediocre way and that results in a mediocre claim. And that's not good for the contractors. So we were really getting rid of, A, poor photography, and B, automating an extremely cumbersome and disliked action by these contractors. - Let me add a little bit more on the measuring piece of it. Because I truly found it fascinating was okay, so that was kind of the phase one. And my friend said use these folks for remediation. They're really good, but don't use them as a general contractor, you won't be happy. So at that point, I think that was on a Sunday. I probably called on a Monday, called our insurance agent. And again, this was all new to me of how this whole process worked. But I got in touch, was connected to Travelers, our insurance company, and they said you could use any general contractor that you wanted, but I did ask them for a recommendation in part because I wanted a general contractor who the insurance company felt comfortable with going back and forth, back and forth with paperwork. So I totally got lucky that we love our general contractor and they've now done three floods and they did a remodeling project for us. But probably not the best way to source a general contractor, but it came from Travelers, and totally happy. But what I found fascinating, , is when the insurance adjuster showed up that week, a couple days after the flood, they did Xactimate. So I want to say the remediation company did the measuring using Xactimate, the insurance adjuster from Travelers used Xactimate, and then the general contractor came out and they used Xactimate. And then at some point, the subcontractors came out for the floor coverings, for the now two floors of wood and laminate we ended up putting down in the basement, he did measuring, and the guy that does paint, he measured. And by the way, at some point the adjuster changed for Travelers so a new adjuster got assigned to us. Our project went on for about nine months, unfortunately. And that new adjuster came out, I want to say did Xactimate again. So I was totally amazed was how many times people kept measuring the same space. And I have to think since this was an insurance claim for $41,000 plus that all the time it takes to do Xactimate by all these people has to be figured into what the job cost. And literally it took hours and hours for measuring our three floors with lots of nooks and crannies and bay windows and et cetera. - Yeah, so I'll touch on two topics you touched there. One of them is the redundancy issue that you mentioned. And the other is the cost of this redundancy. So I'll start with the redundancy itself. Why is a contractor going in, taking photos, measuring, and then an insurance adjuster going in, taking photos, measuring? Two reasons, one, the primary reason is lack of trust. There is ultimately an agency problem here where you have a contractor whose best interest is to say the place was huge and the damage was extensive and an insurance adjuster which interest is exactly the opposite of that. Or so we thought. More and more that we got into the claims world, you understand it's a little more nuanced than that. The insurance carrier cares about adjusting correctly more than they care about lowballing you. A lot of the money that comes into a claim comes from re-insurers and it's not exactly a one for one kind of sum zero game when they lose a dollar on a settlement. But where they get fined heavily and where they could face serious penalties is if they adjust it incorrectly. And that is why adjusters are so diligent. It's often referred to as the most audited job in America, an insurance adjuster. They've got supervisors on supervisors on outside audits that their adjusted claims will have to ultimately face up against. And not to mention it's an extremely litigious environment that often goes to court and appraisal. So adjusters more than lowballing, they care about getting it right, because it's their job on the line. So there is an agency issue here, and that's the main reason you get a lot of these redundancies. How can we trust that this was a 30 foot by 10 when all the contract has to do is say it was a 32 foot by 12 and they'll make 10% more on this? When you think of the low margin business that is construction, the ability to exaggerate a measurement by so little and that's something that even today with the adjuster going in, it's very, very hard to verify. The level of measurements adjusters do is not that of a contractor's often. So it's a very touchy issue. And another one that Matterport helps tackle. It's one of the reasons insurance carriers love Matterport and mostly are glad to pay for that scan done by the contractor is they know that now they have a machine based 3D model and it's not the subjective measurement that the contractor took. Same thing with photos. It is easy to fake photos these days and it's easy to omit the photo that would show and let's say a bad angle over bad light that the damage was not as extensive as you claim it was. There is no way to manipulate or fake Matterport photography. You get everything that is there, whether you like it or not, as often REALTORS will find out. So that element of kind of can't manipulate, can't change, which often folks complain about in our more promotional verticals where they would like to touch up the photos and add things is actually one of the biggest advantage we have in the insurance space where that documentation is bulletproof. So we eliminate the need for that redundancy in many cases, and what that does to the insurance carrier, I'm speaking mainly for the benefits of the contractors, but when you think of the insurance carrier, a buzzword in today's insure tech landscape is what's called low touch and no touch claims. You have these digital insurers like Lemonade and Next and Hippo coming into this space marketing to millennials and saying, take a photo with your phone, you're insured. Oh, you have a claim? File the claim with your mobile app and Lemonade boasts that they've settled the fasted claim ever in the history in about three minutes they settled a $2,000 claim. And they put this on all their marketing. So time to close a claim is a huge sticking point for customers. And traditional carriers are now faced with the fact that, hey, we can't wait three days till we send an adjuster to Dan's house. That's a long time. Dan's going to get disappointed. He's going to badmouth Travelers online. We want to get him settled fast. But if they've got your emergency response person going and scanning Matterport, they'll do what's called virtual adjusting or desk adjusting, remote adjusting. These are terms we didn't make up. Gladly for us, the drone folks got into this insurance space before us and have pioneered kind of the idea. Today Allstate never goes to a roof claim Roof claims are about 50% of claims, property claims. Mostly coming from hail. And today Allstate will send a drone photographer from the neighborhood similar to an MSP network, using a drone base or other drone pilot networks, send them over to your house, they'll fly the drone, the drone will produce a 3D model as well as a visual documentation of your roof and a desk adjuster will sit at their desk and adjust the claim remotely. So we didn't invent anything in the world of virtual adjusting but we were the first to enable this for a large loss interior claim. - It seems like an amazing thing, because I mean, the general contractor that came out, again, I was lucky. The owner of the business happened to be the one that came out, 30 person company, and so our confidence level in this whole discussion was super high. But that said, I was really surprised that someone so senior was doing this Xactimate thing and taking the pictures. And I'm saying hey, David, I got this 3D model and it has all the measurements in it and he looked at it and he said, wow, that's really, that's cool, but this is what I do and this is what the insurance companies expect. And I'm sure that'll be great for the next generation of people like me, but my level of sophistication is I do email and I have voicemail and I'm just kind of a low tech person. So I was like, ugh, but I got something that seems like it would save everybody all this time in the whole process. - So Dan, I mean, as leading the go to market in this industry I can tell you one of the less easy aspects of going to market in the insurance industry is the, I guess, inertia and this is how things have always been done kind of mentality. That exists in every industry. But having gone with Matterport into the architecture and engineering space, taking us to market in the construction space, the facility space, the mortgage appraisal space, and then most recently and we operate, by the way, other than in insurance claims also in insurance underwriting and risk. Having gone into all these spaces, the insurance field is one of those that is I guess most plagued with that kind of mentality. And it's definitely an inhibitor to disruption but not a blocker. As most will tell you, about this time last year, there were about 500 scans done amongst for insurance claims. We're nearing 8,000 today. So it's not stopped us. And this disruption is happening at very high pace. We hope to be at 80,000 a year from now. - Yeah, that's awesome. This seems like such a ripe opportunity to disrupt a space in such a positive way. Speaking literally as a homeowner that went through this process and I'm watching everybody measure the same space over and over and over again and taking pictures of the same stuff over and over again and then oh, by the way, it's the back and forth. So my general contractor says, well, they've approved this, this, and this, but they've disputed this. So we got to take some more pictures. Are you going to be around? We're going to come out and take some pictures. Oh, the insurance adjuster wants to come out again. I really think we probably had four different visits by the insurance adjuster. And I'm going, well, okay, well, I don't know, well. And I can understand some of it. Because when they opened up the wall in the living room by the remediation company, when we finally got to the restoration part, it was obvious that the two by four problem continued further. So they really need to open up the wall more than what was done originally. So somebody from the insurance company wanted to come out, I guess, and verify that even though they took some more pictures that the wall was opened up, that that really needed to be done or something. - Yeah, so I mean, you touched on another important topic that is the return visits aspect of it. So everything we talked about, touchless claim, no claim, even if you do send an adjuster, which often you will even from a customer service perspective, for a large loss, you might want to have somebody there. The house just burned down. You might want to have someone there regardless of the settlement of the claim. But even so, we discovered that on large losses over 50% of claims will get a second visit and about 30% will get a third visit. - Is that crazy? Is that just unbelievable... I just find that amazing. What couldn't you get done? - Well, it makes sense when you have missed measurements and missed photos, but with Matterport, you never miss a measurement, you never miss a photo. You capture everything and you measure everything and if you missed a measurement, you just go back to your workshop and grab that measurement. Just to touch a little bit on measurements, because having gone to market with Matterport in different markets, accuracy is changes in requirement based on workflow. If we're estimating, the [Matterport] Pro2 is definitely within accuracy, within estimation grade. So that definitely makes it a lot easier than other spaces where for some things it works, for some it doesn't. So you touched on the return visit aspect, but I want to take you back to that contractor. And you mentioned something very important. Why is this very skilled person, and I'll tell you this, the estimator in a restoration firm is paid between $50 and $100 an hour. Everyone else on that team is paid minimum wage. The guys ripping out your drywall and the carpeting are paid minimum wage. Why is this person who is the most accredited, experienced, and skillful person on this team taking out a tape measure and measuring things for hours and sketching in software? - It seemed kind of backwards for me. I mean, maybe it's obvious to me, but I'm thinking, okay, this camera, the Matterport Pro2 3D Camera that you mentioned, it scans and it has literally all the dimensions, all the photography. It seems like it would have everything that anyone in this whole conversation needs from the remediation to the renovation to the general contractor. - Other than the scope. What we don't do, and I stress yet, is through AI eventually but currently what we can't do is you scan the room and I'll tell you all the line items that are needed. That estimator, that's where he's needed. That is truly his skill set. Because you look at a damaged room, you see a damaged room. They see 75 different line items. And that's why they're paid that much, because they're the ones writing the bill for the insurer. - It didn't seem, I mean, it would seem like that could be a remote job. Why does somebody have to do the estimate in the house when you have the Matterport scan? It seems like you'd have everything you need in measurements and documents. - And what you say right now leads me to my next point of not only are you able to give the camera to one of your low cost, minimum wage employees that can go and do the scan. And keep in mind, this is not a scan that needs to be very aesthetically pleasing. Your listeners who might be thinking, how can you give this $15 an hour high turnover, low skilled employee a Matterport camera and expect a good scan? Well, it doesn't really need to be a good scan. You don't need really good visibility and going through the doors and making sure the lighting is correct. That's not really what you care about in this setting. So really anybody can do it. And then you say, wait, not only am I taking that task out of his hand, now all they need to do is scope, write in those line items. Why don't they do that virtually? And a huge thing that, like I said, when we started going to this market, we gave the [Matterport] Pro2 Camera to estimators and project managers and said, here, make your life easier. Measure automatically, take photos, don't miss photos. It's very easy and it's very fast. What more and more we saw as customers had this is saying, wait, now I can get to three times more homes because my limited bottleneck resource is that estimator and in a catastrophe event. We have a customer up in Chicago. Last February, polar vortex. They said within a week, 1,500 jobs landed on our table. They're used to this, this industry is used to this. 50% to 70% of annual revenue in this industry comes from catastrophe events, not your every day water losses. So these companies, it's not a new thing for them where they suddenly have a peak of work. But what they can't do is always be set up for that peak in terms of fans, dehumidifiers, blowers, team members, labor. So they handle whatever they can and they hand off whatever they can't. But if your biggest limited resource is that it's hard to scale, is that estimator. Not a blower or a dehumidifier, which you can easily rent from Hertz or Sunbelt Rentals and all these companies. It's that or a fan that you could rent. Or even a camera. All of that equipment can be scaled quite fast, but what you can't scale is that skilled resource. But for them, for our customer in Chicago, this was Chicago Water & Fire [Restoration], we did a case study about them. During that polar vortex, were able to handle 20% more jobs, which translates directly to revenue. Just because they were able to have their estimator sit in the office and there are low cost employees out, they have over 50 Matterport cameras deployed, and all they're doing is scanning these frozen homes and moving on. So the mitigation crew is there left fixing, but as soon as they've got that scan, they have everything they need to do to build. And that's what they care about. - I imagine if you're scanning in Chicago, you're also probably glad that you can get in and get out a lot faster. Because I have to think that using the Matterport scan is going to be far less time on site for anyone that's doing that documentation. So just, again, thinking about, okay, David's walking. Dan, I'm going to be a while. Oh, David, that's fine, I'm just working out of the house. That's fine, okay, a couple of hours later, well, in Atlanta, we don't have any issues with cold and obviously we didn't have a fire, so we didn't have open walls, et cetera. But I imagine if you've got either water damage in Chicago or fire damage in Chicago or both, it's cold, and if you're trying to do Xactimate, that just seems crazy. - Yeah, yeah, no, it's definitely also a matter of convenience, and like you said, time on site. I guess what I'll emphasize is whose time on site. It might extend by a half hour the time needed on site from someone who's there fixing the wall. But frankly, he's going to stay there well beyond the scan, so you're not really extending his time. The estimator, on the other hand, that you can get to visit once and once and not have to return to the site, so you're saving drive time, not only time on site, but you might have him skip going to the site altogether like we said and in that case you're highly decreasing your expensive labor's time on site and drive time and slightly increasing your low cost labor's time on site. So it's a very easy math. But we touched on this a little bit. There are benefits well beyond just the contractor. There are benefits to the insurance carrier. And where that's important is if you ask most of these, like we started with your story, there's two ways this happens. One, you call the restoration company. Two, you call the insurance carrier and they assign restoration. What that means is that this restoration contractor is highly dependent on insurance carriers liking them, having good relationships with the adjusters and their area is crucial. It's literally mission critical for all these companies to exist. And when you send a Matterport documentation and a Matterport created measurement sketch and we now deliver that just as a side note. You can order a full Xactimate sketch. Roughly costs $250. Just like we deliver that $50 floor plan, we deliver a $250 up to 4,000 square feet sketch. - Take a moment and talk more about that, please. - Yeah, sure, so what we realized very quickly and I think what you're going to see is this is the way Matterport is going in general is why are we, if folks are downloading our $50 floor plan and then that gets them 70% of the way there and now they're plugging it into Xactimate and creating an Xactimate sketch, why don't I just deliver them the Xactimate sketch? I'll do it at scale, I'll power it with AI, and I'll do it in a lot more cost effective manner that allows me to make a profit as well as a contractor to save potentially half his in house cost for producing that sketch. So it's a win-win. So we do that. - This is super exciting, but I think it kind of begs a couple questions. So does the insurance, does the general contractor make less money or whoever? Because if you're the general contractor and that used to take you two and a half hours but now you can get it for $250, is that? - So ultimately, if you bought it for $250, you can upsell it as a service. So most of these guys, what they're doing is they're actually making a higher margin, because their time and material cost for doing this, there are certain regulations around that in terms of what you're able to price. Because if you think about it, sure, why doesn't the contractor just take 10 hours to do it and make even more money? So there's a limitation to the G&A that they could fit into on a claim. But if they say now I've gotten this service from an outside vendor called Matterport, that is something that they can, just like any subcontractor service, you mentioned painters. So your mitigation contractor can hire a subcontractor as a painter and make a margin on their service. So there's more opportunity for actually margin, because now they charge $300. We charge $250 for that TrueSketch. They can charge an extra $50 or so and that's actually margin that they can make. But the other aspect is the opportunity cost. It's not only am I making money off this TrueSketch, but now I have seven hours that I would have had an estimator doing that sketch that are freed up for me. So you're not only making it back up and now you can get to 20% more claims. - You mentioned the 1,000 claims in Chicago in a short period of time. I can't imagine that they had enough adjusters. - [Tomer] Estimators. - Estimators on staff to be even able to do the Xactimate. So it sounds like you solved a real bottleneck. - And even not in catastrophe events, Dan. I mean, even on the day to day, this could mean that they're able to, who knows, maybe even reduce their estimating staff from three to two or from three to one, or alternatively say, hey, now I've got one highly skilled estimator and what a highly skilled estimator often means is a good estimator will see 50 line items in that broken room. An excellent one might see 70 because of their knowledge of the software. Maybe have him in the office reviewing the novice estimator's claims virtually. So there's a lot of training possibilities here that open up, a lot of quality assurance possibilities that open up on top of these kind of remote virtual capabilities opening up. - Let me ask you a tactical question in there. First, I've forgotten the name of what you call that product or service. - A TrueSketch. - [Dan] A Matterport TrueSketch. - Yes. - On the Matterport TrueSketch, how long does it take to deliver that? - So we're in beta with it. It is currently a two business day deliverable. We're hoping to get it down to one day. Time is extremely critical in this industry, more so than any other space we operate. I mentioned that the carriers have big overhead when they have a claim in their pipeline. Carriers often put pressure on these contractors to turn claims around in a matter of days. Small claims, it could be a matter of hours. So we're constantly working to improve the turnaround of TrueSketch knowing how time sensitive it is. - And what were some of the claim adjusters, did they ever work with MatterPak? Or no, no, they always worked with the 2D? - No, they've worked with our schematic floor plans or with the TrueSketch. That's really the two alternatives. Sometimes on small claims they won't do either. Like I said, in a room where you could easily estimate or even just use workshop to get wall to wall measurements, that's enough. - So they might take the floor plan view in a Matterport tour and literally sketch over the top of that? - They could do that. There are issues. We fell like in small claims, they often do that. In larger claims, they want to get it as tight as possible. It's part of their claim. I mentioned having insurance carriers like you is mission critical, and that's something we help out with a lot. Because versus poor photography and human error prone and exaggeration prone sketches, now the carrier and the adjuster specifically is receiving bulletproof content in the form of a Matterport scan. Guess what job in that region where that job is going next? To that contractor that used Matterport. And that is by far one of the things we hear across the board from our customers in this space is this thing is getting me more business. And we love to hear that, because that's the... When you talk of value proposition, saving time is great, saving money, saving drive, you talked about convenience, that's great. But when you're talking about getting more jobs or in that example that I said you're able to get to more jobs, that's where your value prop turns, in my opinion, having gone to many markets before, that's when your value proposition goes from nice to have to must have. - Tomer, talk more about that. What are all the different ways for someone in this space to make money? Whether that's a public adjuster or a remediation company or someone that's doing restoration. Where's the opportunity to make more money? - Yeah, so I went over two of those. And again, you touched public adjusters. That's a little bit of a different beast. Public adjusters for those of you on who don't know what that is, there are several types of adjusters in the world. One is the insurance adjuster. They are staff, organic staff of that insurance carrier. Often they're either desk adjusters or field adjusters. Then you have what's called independent adjusters. Those are outsourced adjusters used by insurance companies. So they're anything but independent, but that's their name nonetheless. They work for the insurance carrier. They're an extension of that insurance carrier. Main reason that they're needed is that like we mentioned this industry is prone to catastrophe. And Allstate can't have 10,000 adjusters in the Houston area but suddenly Hurricane Harvey hits and that's what they need. So they'll hire these outsourced adjusters as well as in areas where they have low policyholder coverage and they don't want a staff member there, they'll hire outsource. And then the third type of adjuster is a public adjuster, and that is the adjuster that works for the policyholder. They're an adjuster, which means they're an expert in insurance policy, but they're on your side. These are also big customers of Matterport. And the main reason is they also have to sketch and document, but then they have to go to mitigation. Often they're used in claims where there is dispute. You don't bring on a public adjuster if there's a very clear cut case and your insurance carrier is going to cover it, no questions asked. That's usually not when they're brought in. They're brought in when there's a question of coverage, an extent of coverage, and under-insurance and all of these edge scenarios. It's usually around 10% of claims, 5% to 10% of claims they're brought on. When they are brought on, by the way, claims settle for 20% more. So highly recommend using them if you're in a disputed claim. But these public adjusters, basically, have to tell a story. They use Matterport for storytelling and negotiation. Because ultimately, they'll stand in front of a third party appraiser or a judge or a jury or an investigator and they'll have to tell their policyholder's story. And telling a story, as we've been told many, many times by these public adjusters, telling a story becomes 10 times easier and more persuasive when you have Matterport at your side. And that's what they're using it for. They're using Matterport to win cases, to settle cases. Very different from a restoration contractor, which is using Matterport to file a claim. Document a claim, communicate on that claim to their insurance carrier. - So for the remediation company, where is the opportunity to make more money for a remediation company? - Yeah, so all the things I mentioned, you're lowering time on site, you're lowering return visits, you're lowering visits altogether, you're doing things in a remote fashion. Another big thing that I touched on is carriers will like you. Your relationship with insurance carriers will improve. What I didn't mention is that often mostly on the commercial property side, most commercial property owners, property managers, facility managers, they are targeted directly by these mitigation firms. You go to them and say, hey, here's my card. If you ever have a loss, head of this university. And universities, for example, that span huge campuses, they experience five to 10 losses a year. This is something that's constantly happening. A little fire, electrical fire, flood, window was open, this whole server room was fried. They get losses on a constant basis. Vandalism, theft, a lot of cases. So they're actively targeted. What we've been seeing contractors do and go say, hey, I will scan your facility for you, and I'll get to this use case on the policyholder side in a second, which is inventory documentation. Very important piece of this. But they go in and say, I will document everything in your property for the case of a claim so you have an easier time inventorying. And now here's my card. Use me for any loss. So we've heard that not only do you build relationships with carriers, which are huge constituents, but also you build relationship with property managers, commercial property owners in your area. Huge for these guys. And then one last piece that we constantly hear from our customers is what's called breakage claims. Often when your contractor's going into your house, Dan, and doing things there for the span of nine months, in about I think I heard one in five cases, contractors will come and tell me, hey Tomer, about one in five cases, I have a customer come and tell me, you scratched my fridge, you scratched my hardwood floors, you broke my driveway cement, so many different claims. Now, you have to keep in mind this person, policyholder, sometimes under distress, losing a lot of money, maybe they were under-insured, maybe there was court cases happening. They're on edge. And what often happens is contractors say, I just pay it out. I don't want heartache. I don't want this guy going to the insurance company telling him that my contractor screwed me over. That's not what I want. I just, you know what, here's a new armoire, here's a new fridge, here's a new... We'll fix, we'll paint over that, we'll do it. And I take the loss myself. What they tell me now is, Tomer, I go in first thing I do is I Matterport scan. And then anything that the policyholder tells me, oh, this was that, you did this, you did that, I have perfect documentation, especially with a Pro2. This is something that Pro2 users have told us consistently. The level of zoom I can get to, I can see a scratch in the wood. And then not only do I not pay it out, but I've got great relationship going on with this customer who says, okay, you're right, totally my bad. - So that's coming from the scan that was done before the remediation even began? - Yes, yes, that's from what we call the pre-mitigation scan. Now, keep in mind contractors scan at three different points in time using Matterport. The first time is that pre-mitigation or FNOL scan, First Notice of Loss. The second one is after the mitigation job has been done, which means they dried up the water, they took down the drywall, they pulled out the carpeting, they removed furniture, all that stuff. And then a third one post repair, post restoration, and that is after the house has been fixed. That's basically the three stages that are critical for the contractor to document in order to give to their insurance carrier and say, this was the damage, this was the work I did on the mitigation front, here is the quality of work that I did on the repair front. Pay me. - So are any of the renovation companies using the before and after as a way to get business, to differentiate themselves, to make... - You know, I'd say renovation is a broader category than specifically remediation for insurance purposes. For insurance purposes, they're doing this both as a record for here's the policyholder, here's your new house, go use this Matterport scan to sell your house maybe. But they're also using it for self serving reasons like they need, here's an interesting fact. When you have an insurance claim against your house, it's actually also against your mortgage company's asset. So the mortgage company, in order to allow this contractor to get paid by the insurance company says, wait, I need to sign off that the repair was done here and kept the asset valued what it is, because I own 70% of that asset. So often you need a mortgage inspector to come to your house. But the mortgage inspector is in no rush to come to your house. So you might be waiting three weeks, four weeks, five weeks to get the money from your insurance company just because the mortgage company hasn't inspected. With a Matterport scan, send it over, they clear the inspection and get paid right away. - Very interesting, because thank heavens, our mortgage is paid, so this is a whole nother topic. We didn't have that layer of complexity. But had we still had a mortgage on our house, we might have had to wait for the completed documentation to go over to the mortgage company for them to sign off on it? - Yeah. - Wow. - Yep, you have to wait for it and contractor has to wait for it. And for you it might be an extreme heartache. For contractors, you talk to them, they have huge liquidity issues in this industry. Often getting paid plus 90 plus 120. So these are horrible payment terms from the insurance companies and delaying that payment by another three, four, five weeks often puts them in a cash crunch. - So as your business grows, you're at risk of going out of business because you're... - Like many businesses. Like many businesses, the bigger you are, the more you're leveraged, the more loans you need for your bank to work in capital loans. - Are you hearing from the companies that this is helping improve their cash flow because they're getting paid faster from the insurance companies? - Getting paid faster, not only because of that mortgage aspect, but they're getting paid faster because their time to settlement is faster because there's less disputes. That's probably the key source of speed that we add. They're getting paid faster because their time to file that claim has gotten faster. So they're filing claims faster. They're spending less time in disputes, and they're getting inspected faster. So all these elements add to just a much faster getting paid period from the contractor side. What I like about this is that often we go to fields and we improve different people's lives, I feel, Matterport. In this case one of these kind of indirect effects is the benefit to policyholders. I mean, policyholders, and this is a good leeway for this next little bit, but policyholders getting to their homes faster after catastrophe events or getting to their businesses faster, factories opening up faster, any kind of property loss that is mitigated and settled and repaired faster for me is a huge net benefit to people and to the economy. So I feel like that's an amazing thing that we're able to do here. - Yeah, our project took nine months, which I think is unusual because we actually used it as an opportunity to say, okay, let's renovate the bathroom. Let's not renovate the bathroom after we put down the new hardwood floors. And if there was a happy lining for us, the $41,000 plus change, the insurance and the general contractor and the remediation company, they were within maybe $1,000, and we were only, that came out of our pocket. And that was only because we chose, we wanted to have our plumber, our master plumber, deal with a lot of the stuff rather than the plumber from the general contractor and our plumber cost more. And we were totally happy to have our new hardwood floors because we'd been in the house since it was built, so I think it was, you know, maybe almost 17 years we hadn't refinished the floors. So we're going, well, out of adversity came something good. We got new hardwood floors and we put laminate in the basement instead of the carpet. My wife's happy because we had so much stuff that was wet that she thought was crap anyway. So we threw out a ton of stuff. And so we de-cluttered. - In your case, though, because it wasn't a total loss, you were able to stay living in your home. Think of often folks who are living in alternative housing or hotels around. That's a huge cost to the insurance company for sure, and that's why they want to reduce that cycle time. But it's also just a huge inconvenience. - I think we had to step out of the house for seven or 10 days that the insurance company put us up at a hotel while the hardwood floors were being done. There was a moment where it was kind of depressing, because all the furniture on the main level of the house had to be removed in preparation for the hardwood floor. So I think we literally had two lawn chairs and a TV set and were watching TV, we're looking around and going, well, this is kind of depressing. But at the end of the day, we got some new floors out of it. We were happy. The process seemed to work. I just thought it was the most inefficient process of you can take your picture, come back and take more pictures. - We're trying to get efficiency in there. Yeah, so you touched earlier on policyholders, like in what policyholders service, where the policyholder gets benefits for. But one thing, we touched on these three points in time, first notice of loss, mitigation, and post repair. There's another really important point in time and that is before the property was damaged. Insurance carriers would love to get their hands on your property a second before it was flooded, because most of what's called insurance fraud is because you go and say, hey, this was like that, this was brand new, this was mahogany, this was stony, and basically when you inventory your things and anybody who's gone through a loss can say, especially a fire loss, where the things that were there are no longer there, is told, go inventory everything you had in your living room. And not only is this an extremely painful process, you don't really know, and you're gonna miss 30%, so you're going to be under covered by 30%. And it's just a horrible, nightmarish situation for home owners to go sort through the ashes literally. - So who's the business opportunity for the documentation of the house prior to a loss? - Yeah, so we're engaging lots of insurance carriers, and the carriers are telling us, sure, I would love to have that scan. But for home insurance, then I'm going to take, I don't know, $1,000 in premium a year. I'm not sending anyone over to cut into my margin by 30% with a $300 scan. That's not what I'm after. I'd rather just go based off satellite imagery, given value, and take his word for it in the case of a claim. Not the case so much in commercial properties where they do inspect. And that's kind of how we plan the insurance underwriting space is we say, hey, we could send potentially a scanned service provider to that commercial property to scan it, get an inspection done, you have full inventory of the situation pre-loss, and your underwriting department now has much better data to underwrite with. When you think of underwriting, it's composed of two factors. What is the value of the property I'm underwriting and what is the risk associated with that property? You match those two, you'll get a premium, and that's what underwriters do. That's what the actuaries do in the insurance companies. - Is that an opportunity for the renovation company? - No, not so much. Well, partially, and I'll get to that in a second. But this is basically the need. The need of the insurance carrier, both if there is a claim that need is even more so, because now they really want to know what was there. But even in the onset when they're just insuring or re-insuring or re-inspecting the property, they want to know what's there and what's the risk associated with it so they can better give you a premium and that you won't be underinsured. That's a huge risk that you carry is if you say your house has $10,000 worth of goods and that's now you're happy because your premium is lower but then there's a fire and you start adding things up and you say that's $70,000 of things, carrier goes and says, well, your policy only covers for up to $10,000 worth of goods. Why'd you tell us there was $10,000 in there? So it's in both sides' interest, often, to get appropriate insurance. And retroactively, you would have said, of course I would have paid an extra $10 a month on insurance if I would have known that I wouldn't be losing out on $60,000 on this loss. So often it's in both sides' interest to get the right amount of insurance. Now, where is the opportunity here and for who it is? There is a big opportunity, especially in areas that are prone to disaster. So whether that's northern California where I am right now or southeast Florida panhandle, the Texas coastline, the Midwest, flood prone areas along the Mississippi. Those areas especially when you're talking high net worth homes. But generally homes that I say high net worth, that's where we see the most business pick up for this type of offering. But actually going out and saying, hey, knock on doors, hey, you've got $1 million worth of stuff in this house. Do you really want to risk the case of a flood or fire, taking this all out, and then getting paid low-balled by the insurance not because they don't want to pay just because you don't have any proof? Do you have receipts or pictures? That's the first thing the insurance carrier's gonna ask you. And if not, then they'll go and give some kind of settlement that's somewhere in the middle. We don't believe that armoire was worth $5,000 in terms of the quality, here's $1,000. And that's what you'll get on a lot of your claim. Unless you have really good photography capture of everything there. - So it sounds like you've transitioned, perhaps, to opportunities for Matterport Service Partners? - Yeah, we're seeing... - And that sounds like the first opportunity is documentation prior to loss. - Documentation prior to loss especially in storm and disaster stricken areas, especially in high net worth residential. What we're also seeing is a lot of our contractors, like a lot of our restoration contractors, like I said, offering this to commercial owners. They're less focused on residential except, again, in the high net worth arena. So basically, that's one opportunity is going to commercial and residential properties, high net worth especially, and offering that kind of inventory service for the case of a claim. Now you have something for your insurance to show your insurance agency, to show your carrier in the case of a loss. Another big opportunity is I mentioned this industry being extremely centered around disasters. Often you'll see folks, 70% of my annual revenue comes from the two months of winter and specifically one or two or three big storms. That's something that you often hear in this industry. And this industry is very used to supplementing. And like I said, that's labor supplementing, supplementing with vehicles, supplementing with hardware. What they would often like, and we've seen this and I've talked to several MSPs who have done business like this, is say, go reach out to your local restoration company. They'll likely not use you for the day to day Matterport scanning because they have cheap labor, they're already going on site, and they're very used to lugging around hardware. Their trucks are full of hardware. - It's also 24/7 on demand. - We're set that they need in emergency. But in the case of a storm and now suddenly there's a flood, there's a hurricane, I guarantee you, you as a Matterport Service Provider go to that area, that region, call up the restoration contractors and say, hey, I've got a device mostly likely by now if I've done my job well they would have heard about Matterport and they're ready for your call basically saying, of course you're another hand, a working hand with a Matterport device? I've got five jobs for you today. Not only that, but even if they haven't heard of Matterport, your pitch is, I will go to all your losses, perfectly document them, and deliver you an Xactimate sketch all within the next two business days for these next two properties. And they'll say go, basically. So that's the other element of big opportunity is I'd say familiarize yourself with your local restoration contractor. Reach out to them. Get them to understand the offering that you have. Often, by the way, they may say, you know what? This seems like a great service and on the day to day use you maybe until they buy a Matterport camera or even afterwards, who knows. Depending on their business model and how much they want to get involved in this. So definitely be able to offer them as an initial service but even more so in the case of a disaster where you say, in a disaster, tell me, give me addresses, and all I do is go hit up these addresses, scan, send it to your estimator, and move on to the next loss. You'll be estimating 10 times more homes than you would having your own estimator going around measuring, documenting, and moving on like that. So it's a great offering to restoration firms in that sense. Same thing with public adjusters. Public adjusters, unlike restoration contractors, are not minimum wage. And they are often not on site as an emergency as much as the contractor. So I'd say there's even more opportunity there. Get familiar with the public adjusters in your area and offer them this service. So I'd say probably in between the public adjuster, supplementing restoration contractors and offering inventory documentation services, those are probably my top three opportunities for Matterport Service Providers. - Yeah, I think I would add maybe one or two. I think if there's maybe a remediation company, a restoration company that's thinking about Matterport but they just don't know, then this might be an opportunity to say, hey, take me with you on some jobs so that you can see the workflow, continue to use your Xactimate, but watch the parallel process of what I can deliver for you. That's not a sustaining business model for the photographer. On the other hand, it might be an opportunity for training and support locally to be training people. - I'd say it is an opportunity, because even when that contractor buys that camera, you are their go to supplement. So actually going around and saying, initially, I will offer Matterport services on your losses until a point where that contractor says, hey look, this is amazing but I need more availability of the camera and I want my team with it and I want it to be readily available to me and I'm okay with hardware costs and the training of it. But like I said, suddenly we get 3x more jobs because there was a storm this month, and I'm not gonna go and buy two more Matterport cameras and then sell them. So that's the idea of supplementing. The best way to get in your contractor's supplement pocket is by initially offering a Matterport service until they buy. So I think it's a sustainable model. - I could imagine the company you were describing in Chicago that has now bought 50 cameras. At some point, somebody had to train the people and there was an opportunity for some company to being doing training and support and handholding. So I think that's an opportunity for Service Providers. I think demonstrating what Matterport can do. Given that there's three places that someone scans, which is 24/7 within an hour of that fire or flood, that's not really an opportunity for a service provider, nor is documenting after that remediation of here are all the blowers, dehumidifiers, devices, et cetera. Maybe for the after fact. But again, I think that's probably a general contractor that now already has a camera. So I still think that the training and the emergency if there's particularity in California or the panhandle, someplace in Florida, maybe hurricanes, fires, flood, it seems like there's a whole lot of business there and that probably is not a business that is going to be a lot of pushback on price when the general contactor all of a sudden has 1,000 opportunities, it can only handle half of them, those other 500 is found money. And I would imagine that the scanning is going to be a very profitable business for the service provider as well as marking up the, forgive me, the TrueSketch. TrueSketch? Even if the service provider's paying $250 for the TrueSketch, it's still an opportunity to mark that up. - Yeah, either mark it up or just use it as, like I said, as a leads generator. That's what's going to get the contractors extremely interested is when you say you can deliver a full Xactimate sketch. They know that there is... Today in the world, there are 34 Xactimate certified trainers. That's an extremely coveted skill set. So for you to come off the street and say, I'll deliver a perfect sketch in two days is often mind blowing for these guys. - Yeah, it's crazy exciting. Before we wrap it up, I just have a couple other questions. I know we have some folks that have been patiently standing by in our green room. If they could just keep typing the questions, I'll see if I can get to them in the notes I'm looking at. Tomer, I'm just wondering, if this is such an amazing thing for the insurance companies, do you think we'll be at some point where it's just the requirement if you wanna do work for Travelers insurance, you're going to be expected that the claim's going to be filed, the three phases of documentation is going to require a Matterport or something similar? - Yeah, I'm working on it. It's definitely a big part of my role is to, I'd say, almost act as an evangelist for Matterport at the insurance carrier level. We were on a call with we're all extremely NDA-ed in this industry, so a major top 10 carrier. And this is our first call with them. And this is with a VP of claims and some pretty major folks in that organization. And as we kick off the meeting, I say, okay, well, maybe let's just align here. Does everyone know what a Matterport scan looks like of a claim, should I pull it up? And the head of claims tells me, oh no need, I've actually given a presentation on Matterport to our adjusting staff. And I say, great, where did you hear about it? She's like, where did I hear about it? Over the past six months, we've received here at X insurer over 300 Matterport scans from restoration companies. Our adjusters love them. We don't even need to pilot Matterport. They're already going into, okay, how do I get an account so I can have models transferred to me for storage, for safekeeping post scan? How do I get... Give me a network of the contractors using this. I'd like to engage them and prefer them over others. Give me a list of service providers so if there is no contractor with a Matterport in the area, I can solicit an MSP. So we're facilitating all of that. We're not doing technically any direct selling to carriers just yet. Because really what we're trying to get them to do is adopt the medium. Currently I'd say we're not yet at enforcing a Matterport scan, but we're definitely at the stage of incentivizing a Matterport scan. When an insurance carrier that's a top 10 insurance carrier tells the world that they prefer Matterport scanners over non Matterport scanners and contractors, that has a big effect on what contractors do. - Yeah, this is awesome. What are you doing talking to me today? You should be out there talking to all the major insurance companies, creating that demand for the entire pipeline. (Continued below ...) |

||

| Post 1 • IP flag post | ||

|

WGAN Forum Founder & WGAN-TV Podcast Host Atlanta, Georgia |

DanSmigrod private msg quote post Address this user | |

| (Continued from above) - Yeah, that's definitely a big part of what we do in business development. - It's super exciting to hear. It sounds like if it's not this week, next month, next year, it seems like it's inevitable that the insurance companies for all the reasons that we've been discussing today at some point are going to say, this is the minimum level of performance that if you want to submit a claim to our insurance company, you need to be using this. Or at the very least, we're going to be paying a different rate or a bonus or an incentive because we know we can close out the claim faster, we're going to have less issues in terms of discrepancies for 1,000 other reasons. - And warranty, the ability to capture that repair scan and then someone claiming that the contractor didn't fix what they did fix. There's a lot of benefits to the insurance carrier down the line. I'll also leave you with this thought, Dan. If carriers get more and more addicted to the Matterport medium for closing claims, what about your MSPs which just scanned a home that two years later there was a claim against and now that home is just sitting archived in your MSP's cloud portal? Maybe there's a willingness to pay from the insurance carrier for that. And maybe Matterport can help facilitate that transaction down the line. So there's huge opportunities as insurance and insurance carriers start adopting this for risk, for inspection, for claims handling. Suddenly the other assets that we're creating for who knows, maybe you scanned this restaurant just for promotional purposes, or you scanned this factory for facilities management purposes, or you scanned a home just for leasing or a vacation rental. Whatever the purpose your photographer at MSP scanned it for, now there's an insurance carrier which is heavily interested in that scan. And maybe we can be that market maker, Matterport, and facilitate that transaction down the line. So I think there's a lot of excitement about that possibility happening down the line as well. - Yeah, that sounds huge. As more and more houses get scanned and there's this critical mass. I recall last year when a multi-million dollar house burnt down in one of those horrible fires that that home had been scanned by one of the members of our community. And the insurance company reaction was, wow, I've never seen documentation ever like this before and the claim was immediately settled and there was no issues over what was in the house when it burned to the ground. - Yeah, that's definitely, I mean, we don't see it too far away from today, especially now with the proliferation of 360 cameras and our support of those. Why not even put it in the hands of an agent? And your insurance agent at the point of insurance goes and it's not a house for sale, so they don't need a Pro2 high quality DSLR quality. They just go around with a 360 camera, maybe even without a tripod, because they don't care if they're in the scan and just go around with a 360, create a Matterport model for a 2,000 square foot home in 15 minutes with no tripod. And that's all they've invested is with a $300 camera and 15 minutes of their time and now they've got that capture of the home so if there's a case of a claim, so they can underwrite it better. So I think there's a lot of different places this can go and we're just scratching the surface in this market. - It sounds like it. I mean, certainly one of my takeaways, it seems like, well, okay, there's an opportunity for documentation of high net worth individuals' house or houses to begin with, because maybe at least some high net worth individuals have the dollars to spend. - Yeah, that's a no brainer for them. Spending $200 to ensure, to make sure that you're covered for $1 million worth of artwork and jewelry and things like that is a no brainer. - Or more, or more. So Tomer this has just been a fascinating program. Thank you so much for being on the show today. - Yeah, you got it. Happy to do this. We're looking to create as much opportunity for as much of the ecosystem of Matterport as possible and I really hope MSPs can play a part in this. I do a lot of go to market here and every industry, and I almost put it on a scale of do it yourself, DIY on one side, and service scan service on the other side. Every industry falls somewhere on that spectrum. This one is even one of those that falls heavily on the DIY side and at the same time, there's still opportunity here for services that we outlined. So I think more and more markets we go into, the more success we have in going into these new markets and developing these new use cases, the more the entire ecosystem's going to benefit. - If some of our viewers work in a remediation company or work at a restoration company or even remodeling, remediation, restoration, remodeling related to remediation, restoration, they want to contact Matterport, what's the best way to get in touch? - Yeah, they could email either directly to insurance@matterport.com or go to our website. Under Industries, choose Insurance and Restoration. There's going to be a little video there, some explanation just on the tip of the iceberg of everything I touched on today. But there's gonna be a form there to enter your name and number and someone from my team will get back to you and give you all the information you need. - Terrific, I would add, Matterport has such amazing resources in this category of insurance. I've gone to matterport.com, matterport.com, looked under the category of insurance. I filled out a form. I got to see an hour long program that you did with the gentleman in Chicago. It was a great interview. I thought it was a lot of great insight. And then in addition, Matterport has done some terrific case study, I would call them case study marketing videos. And we've published all of these in the We Get Around Network Forum. So if you come to WGANforum.com ..., search the box for insurance, you'll pop up all these videos that tell the story firsthand from remediation companies, from restoration companies. So really great resources. - Yeah, those are great. Definitely recommend that as the resource. The stories that matter, we've got some great folks here at Matterport in the past I guess six months that have really beefed up our content game in all the industries. Across all our industries, we felt like we weren't telling the compelling stories that our customers have with Matterport and wanted to get the word out. So yeah, just a shout out to our content team here. Doing a great job on videoing these stories that matter and getting it out there. - Yeah, lot of great video. And also you mentioned that case study on the Chicago company, kind of a one page PDF which is also available. You go to matterport.com, you go to the Insurance tab, the tab for verticals, select Insurance, and then just enter your email address and then boom, you instantly have it. So my apologies to some in our studio audience. I think we've just gone long today. If you post the questions in the We Get Around Network forum I'm sure we'll get some answers for you all. Tomer, thank you again for being on the show. Just awesome. Who knew my loss, my wife and I having a loss of $41,000, fortunately getting reimbursed for it, would turn into an interesting conversation of understanding the backstory of where Matterport kind of fits in. - Yeah, I didn't know I would know a lot about restoration and contracting going into this job. So I'm often pleasantly surprised as well. So thanks a lot, Dan. Yeah, really great having this opportunity to speak to your listeners. I hope I could bring this kind of content, keep bringing you guys new markets, new uses that we're going into, new spaces. We're developing new capabilities all the time and that even expands further our usage. And yeah, thanks for being our partners. - Great, thanks Tomer. We've been visiting with Tomer Poran. Tomer is the Matterport Director of Business Development, Head of Partnerships and New Market Development. New Market Development. Obviously also an insurance subject matter expert. I imagine he's a subject matter expert on a number of things at Matterport. So we hope to visit with Tomer on some other topics. We've been recording today's show. So if you missed any portion of it, we will publish it in the We Get Around Network Forum, WGANforum.com, we'll do that by tomorrow, Friday, November 8, 2019. From San Francisco where Tomer is and Atlanta, Georgia, where I am, thanks again for watching WGAN-TV Live at 5. - Thank you very much. |

||

| Post 2 • IP flag post | ||

|

WGAN Forum Founder & WGAN-TV Podcast Host Atlanta, Georgia |

DanSmigrod private msg quote post Address this user | |

| Hi All, WGAN Forum discussions tagged: ✓ Fire ✓ Flood ✓ Remediation ✓ Restoration ✓ Insurance Plus ... ✓ How to be Certified: Actionable Insights Matterport Certification (AIMC) ✓ Transcript: WGAN-TV: Matterport Meets Insurance Underwriting and Risk Mgmt Best, Dan |

||

| Post 3 • IP flag post | ||

|

WGAN Forum Founder & WGAN-TV Podcast Host Atlanta, Georgia |

DanSmigrod private msg quote post Address this user | |

| Hi All, Our thoughts are with those in the path of the hurricane in the gulf coast region. Safety first; then help others with documentation for faster Insurance claims. Dan |

||

| Post 4 • IP flag post | ||

|

WGAN Forum Founder & WGAN-TV Podcast Host Atlanta, Georgia |

DanSmigrod private msg quote post Address this user | |

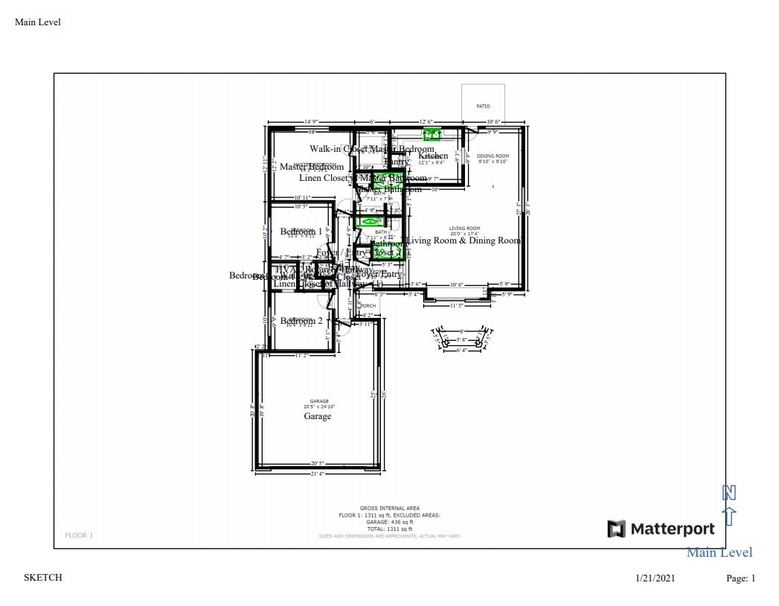

Screen Grab: Get a WGAN-TV Live at 5 Show Reminder via Text Matterport digital twin of a house file. Matterport tour courtesy of Pearland, TX-based A Public Adjuster Group LLC (Randell Smith)  Matterport TruePlan Xactimate Sketch courtesy of Omaha, Nebraska-based Property Damage Estimating Services Owner @Jacek Kazimierz Latarewicz  Property Damages Estimating Services | Contact Us WGAN-TV MSPs: Understanding Matterport & Xactimate for Insurance Adjusting Hi All, How does a public insurance adjuster and restoration contractor use Xactimate and Matterport to help clients receive an accurate estimate on their insurance claim? Why does this matter to Matterport Service Providers? (1. accurate measurements; 2. eliminates sketching a space by hand; 3. eliminates photos; 4. saves money/time related to travel) Now that Matterport offers its TruePlan Service to create Xactimate models, Matterport Service Providers have a powerful tool to offer for insurance claims of properties that have experienced fire and flood damage. Find out much more on WGAN-TV Live at 5 on Thursday, 28 January 2021 when my guest is: Omaha, Nebraska-based Property Damage Estimating Services Owner Jacek Kazimierz Latarewicz (@Jacek): ✓ WGAN-TV | MSPs: Understanding Matterport & Xactimate for Insurance Adjusting Learn the lingo and value propositions from an experienced Xactimate insurance estimator so that you can develop new business with: 1. Public Insurance Adjusters (PAs) 2. Renovation and Remediation companies 3. Insurance companies 4. Law Firms (litigation of property damage) 5. Claim consultants for insurance companies ($1+ million claims) 6. Other companies that find the Matterport TruePlan Xactimate helpful Jacek will walk us through an Xactimate plan and a Matterport digital twin of a house fire to show how the Xactimate and Matterport tour are used for insurance claims (and why these tools are much better than just photos for documenting claims). Jacek has 20+ years of experience using Xactimate to help policy holders get the most money back on an insurance claim by having an accurate estimate and previously worked as a Senior Xactimate Estimator estimating insurance claims. I met Jacek in 2016 when he helped my wife and I in Atlanta with insurance adjusting for water damage in our home (when we were not getting as much money as we thought we should have from the insurance company). Shortly afterwards, that lead to me doing a Matterport digital twin of a flood damaged home (below) and described in detail in this WGAN Forum discussion (and video below): ✓ Video: Matterport Space Meets Water Damage Insurance Claim WGAN Forum Related Discussion ✓ Transcript: Matterport Webinar: Matterport TruePlan™ (Xactimate) ✓ Transcript: Matterport Insurance Claims: Flood/Fire Remediation/Restoration ✓ Transcript: WGAN-TV | How to (Easily) Add Lights to Matterport Pro2 Camera ✓ Transcript: WGAN-TV: Matterport Meets Insurance Underwriting and Risk Mgmt WGAN Forum Discussions Tagged ✓ TruePlan ✓ Xactimate ✓ Insurance ✓ Insurance Adjusters ✓ Insurance Claims Settlement ✓ Flood ✓ Fire ✓ Remediation ✓ Renovation What questions should I ask Jacek on this WGAN-TV Live at 5 show? Best, Dan Video: Matterport Meets Insurance Documentation (11 June 2016) | Video courtesy of WGAN-TV YouTube Channel | WGAN-TV Live 5 guest - Omaha, Nebraska-based Property Damage Estimating Services Owner Jacek Kazimierz Latarewicz - in blue shirt in the center. Matterport digital twin of a flood damaged home by We Get Around Network Chief Photographer Dan Smigrod |

||

| Post 5 • IP flag post | ||

|

WGAN Forum Founder & WGAN-TV Podcast Host Atlanta, Georgia |

DanSmigrod private msg quote post Address this user | |

| Video: Matterport TruePlan in 30 Seconds | Video courtesy of Matterport YouTube Channel | 6 April 2021 | ||

| Post 6 • IP flag post | ||

|

WGAN Forum Founder & WGAN-TV Podcast Host Atlanta, Georgia |

DanSmigrod private msg quote post Address this user | |

| Video: Matterport for Restoration in 30 Seconds | Video courtesy of Matterport YouTube Channel | 6 April 2021 | ||

| Post 7 • IP flag post | ||

|

WGAN Forum Founder & WGAN-TV Podcast Host Atlanta, Georgia |

DanSmigrod private msg quote post Address this user | |